The Importance of Documenting Your Business’ Pre-Loss Condition

Documenting a business's pre-loss condition is essential for effective risk management and financial recovery. This process involves keeping detailed records of assets, operations, and safety measures to facilitate insurance claims and enhance overall preparedness.

- Pre-loss documentation includes lists, photos, and financial reports that show the business's condition before a loss.

- Having clear records helps speed up insurance claims and reduces disputes, ensuring fair compensation.

- Good documentation practices can lead to cost savings, lower insurance premiums, and improved risk management.

Pre-loss documentation refers to the process of recording the condition and value of a business's assets before any adverse events occur. This practice is crucial as it facilitates smoother insurance claims and provides a clear understanding of the business's worth, enabling quicker recovery in the event of a loss.

Businesses face different risks that can stop them from working properly and hurt their finances. While many focus on fixing things after a problem, it’s important to know what everything was like before something went wrong. This is called pre-loss documentation. It helps in several ways, like making insurance claims easier and knowing the real value of what you own. Having clear records of your business before anything bad happens can help you get back on your feet faster if problems arise.

What Pre-Loss Documentation Means for Your Business

When a business faces unexpected problems like disasters or losses, having pre-loss documentation is very important. This means keeping detailed records of what the business owns, how it runs, and its financial health before anything bad happens.

Pre-loss documentation includes lists of everything the business owns, photos, videos, records of any maintenance, financial reports, and how things are normally done. These records show what the business was like before the problem, which helps in figuring out what was damaged or lost. Insurance companies use this information to decide how much money the business should get back.

This documentation also helps the business find weak spots, plan for risks, and follow insurance rules. It makes the process of getting insurance money faster and easier, helps avoid arguments, and speeds up recovery. This keeps the business financially safe during tough times.

Benefits of Pre-Loss Documentation

Pre-loss documentation helps businesses manage risks better.

By keeping records, companies can spot dangers, decide on insurance, check if they follow rules, and put safety plans in place before anything bad happens.

This can save money by stopping problems before they start, getting better insurance deals, and making it easier to bounce back if something does happen.

Risk Identification & Mitigation

Pre-loss documentation helps businesses spot risks and find ways to prevent problems before they happen. By listing assets, processes, and weak spots, companies can see what needs more protection or changes.

This helps businesses check if buildings are strong, see if equipment works well, and find safety problems that might cause damage. Then, they can decide which risks to fix first based on how bad they might be and how likely they are to happen.

Common fixes include making buildings stronger, improving security, adding backup power, and setting up emergency plans.

Insurance Assessment

According to Risk & Insurance, understanding the role insurance can play in recovery, before a loss occurs, creates an opportunity to integrate your business response and insurance claims process into one seamless protocol. One of the most effective ways to prepare is by keeping detailed, up-to-date records of your assets, operations, and financials. Having this information ready before an incident not only helps confirm you have adequate coverage but also speeds up claims, reduces disputes, and clearly shows the pre-loss condition of your property.

Insurers rely on these records to:

- Accurately assess the value of your assets, operational capacity, and revenue potential using inventory lists, financial reports, and operational documentation.

- Compare pre- and post-loss conditions through dated photos, repair logs, and inspection reports.

- Support business interruption claims with historical production data, customer contracts, and supplier agreements.

Well-organized records make communication with insurers smoother, minimize coverage disputes, and improve the likelihood of receiving a fair payout. Businesses that maintain strong documentation also demonstrate sound risk management practices, making them more attractive to insurers and better positioned for recovery after a loss.

Code Compliance

Businesses need to keep good records showing they follow building rules and safety standards. This is important for making sure their buildings are safe and for insurance purposes.

If something bad happens, like a fire or storm, these records can show the damage wasn’t because they ignored rules. Before any problems happen, having proof that they met all the rules can make fixing things easier.

This proof includes things like inspection reports, maintenance records, permits, and certificates. Having this information ready can help insurance people see that everything was in order before something bad happened.

This can make insurance claims faster and help avoid arguments about whether the building was up to code or not.

Safety

Pre-loss documentation is important for keeping workplaces safe and protecting workers and company property. By keeping track of safety conditions, companies can spot dangers and fix them before accidents happen.

Important safety records include:

- Photos and videos showing where safety gear, emergency exits, fire systems, and first aid stations are. This helps make sure they are in the right place and easy to get to.

- Regular checkups of machines, safety gear, and repair schedules to ensure everything works well.

- Records of safety training, accident reports, and risk checks to show the company follows safety rules.

These safety records prove the company is careful about risks and help keep safety steady in the workplace.

Cost Savings

Detailed records before a loss can save a lot of money. They help lower insurance costs, make claim processes faster, and help avoid arguments over payments. Companies with good records show they can manage risks well. Insurers like this and may offer better rates and coverage.

| Cost Impact | Savings |

| Lower Premiums | Save up to 15% on yearly insurance costs |

| Faster Claims | 40% quicker claim payouts |

| Fewer Disputes | Cut legal costs by 75% |

| Less Downtime | 30% reduction in business downtime costs |

| Less Work | 50% fewer staff hours spent on claims |

Having records before something bad happens works like a money guard. It stops fights over how much things are worth and keeps business running smoothly. Companies save money because they don’t need extra help from outside experts. This way, claims are paid faster, and the business stays less disrupted.

Asset Protection

Asset protection is one of the most valuable benefits of maintaining thorough pre-loss documentation. By keeping detailed records of your property, equipment, and inventory, complete with dated photographs, receipts, and maintenance logs, you establish clear proof of ownership and value. This documentation becomes critical if your assets are ever damaged, destroyed, or stolen, as it allows you to demonstrate exactly what you had and its condition before the loss.

Not only does this help prevent undervaluation during the claims process, but it also reduces disputes with insurers and ensures you receive fair compensation. In short, pre-loss documentation safeguards the investments you’ve made in your business, making it easier to recover and rebuild without unnecessary financial setbacks.

Essential Components of a Pre-Loss Inventory

A good pre-loss inventory is like a checklist that helps organizations know what they have before any disaster happens. It includes taking clear pictures and videos of everything they own. This means all the stuff in their buildings, like computers, furniture, and machines. They should write down details about these items, such as what they are, their serial numbers, and when they bought them. Knowing how much these items are worth now is important, too.

It’s also crucial for organizations to keep track of how they do their work. This includes knowing what different employees do and how the business runs day-to-day. They need to keep their financial papers up-to-date. This means knowing how much money they expect to make, how much they owe, and how much others owe them.

Digital things are part of the inventory, too. This includes software they use, licenses for that software, and important data backups. They should also make notes about their building, like how the electricity and plumbing are set up, and the overall structure.

All this information helps them know exactly what they have and what it’s worth, making it easier to recover if something bad happens.

Key Areas to Document in Your Facility

When you document your facility, focus on key areas. This helps if you need to make insurance claims or recover from a disaster.

- Outside of Building: Look at the roof, walls, windows, doors, parking lot, gardens, and security systems. Take notes and pictures.

- Inside of Building: Check the floors, ceilings, lights, heating and cooling systems, electrical panels, plumbing, and any special room equipment. Record details and photos.

- Special Areas: Pay attention to important places like server rooms, factory floors, storage areas, loading docks, and spots with valuable or special equipment. Make sure to document these well.

Doing this gives you a clear record of your building’s condition, making it easier to deal with damage and repairs later.

Digital Tools for Asset Documentation

Modern businesses can use digital tools to make keeping track of their assets easier and more reliable. These tools help with collecting, storing, and finding data, while also reducing mistakes.

| Tool Type | What They Do |

| Mobile Apps | Scan items, take pictures, add location info |

| Cloud Platforms | Safe storage, access for many users, and save backups automatically |

| IoT Sensors | Watch conditions live, track changes, log data |

These tools help create a strong system for keeping records that insurance companies and risk managers can trust. Smart features like AI and machine learning make these records even better by finding mistakes and organizing items automatically. Software updates keep them up to date with new rules and safety needs.

Organizing and Storing Business Documentation

To keep business documents safe and organized, you need to set up good systems for storing them.

- Digital Storage: Store important documents online in a secure space, like a cloud. Make sure they are protected with passwords and backup copies. Use tools that keep track of changes made to these documents.

- Physical Storage: Keep paper documents in a safe place that won’t burn, like a fireproof safe. Label everything clearly and keep a list of what you have stored.

- Mix of Both: Use both digital and paper storage to make sure nothing is lost. Regularly check and update your documents to keep everything current and safe.

Check your systems often to make sure they work well and follow the rules. This helps prevent losing important information and makes it easier to find what you need in case of an emergency.

Inventory Management and Documentation Systems

Organizations need to keep track of all their stuff, like tools, supplies, and equipment. This is called inventory management. They need to know when they bought things, how much they cost, their serial numbers, where they are, and how well they work.

A good system uses both computers and real-world methods to keep track of everything. This can include using barcodes, RFID tags, or QR codes to know exactly how many items there are. Regular checks help make sure the counts are right and find any mistakes. Taking pictures helps show what condition things are in and where they are located.

Companies should keep up-to-date records of where items go, how much they lose value over time, and what it would cost to replace them. This way, they have the right insurance, can plan for emergencies, and have proof if they need to make an insurance claim or if something disrupts their business.

Documentation Strategies for Multiple Business Locations

Businesses with more than one location need a good plan for keeping records. This makes sure information is the same everywhere and easy to find if needed quickly, like in an emergency or for insurance reasons.

Here are some key ways to keep documents organized:

- Central Digital Storage: Keep all records like equipment lists and building details in one online place so that all locations can access them easily and keep them updated.

- Location Codes: Use special codes for each location. This helps identify and track items and papers quickly by where they are.

- Regular Checks: Every three months, double-check records at each site. This helps ensure everything is correct and up to date, and that all locations follow the same rules for keeping records.

This way, all locations stay on the same page, and records are complete, reliable, and easy to share or check when needed.

Training Staff in Documentation Procedures

Organizations need staff who know how to document things properly. To do this, they should have good training programs. These programs teach how to take clear photos, keep track of inventory, and save documents safely. Employees also learn to record details about equipment and how things work in the business.

Staff need to stay updated, so regular training sessions are a good idea. This helps them remember how important documentation is for things like insurance and keeping the business running smoothly.

Companies should also check to make sure everyone is following the rules by doing audits and making sure people are accountable.

Legal Considerations in Asset Documentation

Following the law is important for keeping track of assets. Businesses must follow rules and standards to record the condition of their belongings before anything happens to them. Good records can help with insurance claims or in court.

Here’s what businesses need to do:

- Use time stamps and digital signatures to show when records were made.

- Follow privacy laws to protect sensitive information, especially when using the cloud.

- Adhere to specific rules for different industries, like safety records for equipment or guidelines for food service.

Keep records as long as the law says you should. Make sure they stay safe and can be used in court.

Regular checks ensure you keep up with new rules.

Common Documentation Mistakes to Avoid

Many businesses make big mistakes when documenting their stuff before something bad happens, which can mess up their insurance claims or court cases. Common mistakes are not updating documents often, only using digital storage without backups, and having incomplete lists of their stuff.

Businesses often forget important things like software licenses, documents about their ideas, and employee training certificates. Other mistakes include not putting dates on documents, using different names for the same stuff, and not keeping records of repairs.

When taking pictures, people often use bad quality images, don’t use enough light, or miss important angles of valuable items. More mistakes include not writing down serial numbers, not keeping receipts for improvements, and not having clear rules for keeping documents.

These errors can make it hard to win claims or court cases.

The Role of Professional Appraisals

Professional appraisals are important for figuring out how much your business is worth. These appraisals are done by certified experts who know how to check the value of things like machines and tools.

Here’s what a professional appraisal includes:

- Looking at physical things like machines and tools. They take pictures and check serial numbers to make sure everything is recorded.

- Comparing similar items sold in the market to find a fair price. They think about how old and worn out the item is.

- Writing detailed reports that explain how they figured out the value. These reports have data and numbers that follow industry rules.

These appraisals are really helpful when you need to talk to insurance companies, especially when you have unique things that are hard to price.

Certified appraisers ensure that the values they find are trusted and accepted by insurance companies and courts.

Working With Insurance Adjusters Post-Loss

When something bad happens and you need to work with insurance adjusters, it’s important to have all your papers and pictures ready.

Business owners should keep things like photos, lists of stuff they own, and expert opinions safe. This helps when talking to adjusters about what got damaged.

When you talk to adjusters, show them proof of what was broken using your photos and lists. This helps them see how much you lost and makes sure you get the right amount of money.

It’s a good idea to write down when you talk to adjusters, what time it was, and what you talked about.

Be ready to answer questions about what your business was like before anything got damaged. They might ask about how you took care of things or if you made any changes or fixes before the bad event happened.

Preparing for the Loss Before It Happens

Businesses need to get ready for problems before they happen. They should keep track of what they own, understand their insurance, and check the condition of their stuff often.

Knowing what’s covered by insurance and what’s not helps them know if they have enough protection. Taking photos, writing down what they have, and keeping records of repairs show what everything was like before something goes wrong.

This is helpful if they need to make an insurance claim.

Keep a Detailed Inventory of the Property

To keep track of your business stuff, you should make a list of everything you own. This helps if something bad happens and you need to tell the insurance company what was lost or damaged.

Here’s how you can do it:

- Take clear pictures and videos of all your business things. Make sure to get close-up shots of things like serial numbers and models.

- Use a computer program like Excel to list when you bought each item, how much it cost, where you got it, if it has a warranty, and how much it’s worth now.

- Keep paper and digital copies of your receipts, any repair records, and other important papers in safe places. Use the cloud (like Google Drive) or a location away from your business to store these.

Doing all this will help you when you need to make an insurance coverage claim and get back on your feet quickly after something goes wrong.

Understand Your Insurance Policy

To understand your insurance policy, you need to know what it covers and what it doesn’t. Look at the limits, deductibles, and special rules that might change how claims are paid.

Important parts to check are business interruption coverage, property damage, liability protection, and any special add-ons.

See if your insurance policy pays for full replacement costs or just the value of your stuff right now. Also, look for gaps in coverage, waiting times for claims, and what paperwork you need to submit.

It’s a good idea to go over your policy with an insurance expert to make sure it still fits your business needs.

This way, you won’t be caught off guard if you have to make a claim, and you can be sure you’re covered for possible losses.

Document Property Conditions Regularly

Regularly checking and recording the condition of your business property is very important. It helps protect what you own and makes it easier to deal with insurance if something bad happens.

- Take clear pictures and videos of your whole business area. This means outside walls, the roof, equipment, where you keep your stock, and inside rooms. Update these every few months or if something big changes.

- Write down what condition your things are in. Keep notes of any repairs or upgrades you do, including the date and who did the work.

- Scan or take pictures of important papers like receipts and warranties. Keep these copies safe both at your business property and online in cloud storage.

Doing these things helps you know exactly what your stuff is worth and makes it faster to deal with insurance claims if you need to. This way, your business won’t be interrupted too much, and you won’t lose too much money.

Immediate Steps After Property Damage

When something damages a business building, it’s important to act fast to keep losses small and help with insurance claims.

Prioritize Safety and Prevent Further Damage

When something bad happens to a building, it’s important to act fast to keep people safe and stop more damage. Business owners and managers should stay calm and follow emergency plans.

- Get everyone out of unsafe areas. Make sure everyone is safe and counted. Set up a safe zone around the building.

- If it’s safe, turn off things like gas, electricity, and water. Work with emergency workers and utility companies.

- Use tarps, boards, or barriers to protect the building from weather, trespassers, or falling down. Write down what you do for insurance.

These steps help keep people safe and protect what’s left of the building.

Contact Your Insurance Company Immediately

If something damages your property, call your insurance company right away. Most insurance plans say you have to tell them quickly and give you a set time to send in your claim. If you wait too long, you might not get covered, or they might say no to your claim.

When you talk to the insurance company, tell them what happened, when it happened, and what got damaged. If you did anything to stop more damage, tell them about that, too. The insurance company will give you a claim number and tell you what to do next.

Keep a record of every time you talk to the insurance company. Write down who you talked to, when you talked, and what you talked about. This will help make sure they handle your claim right, and you can look back at it later if you need to.

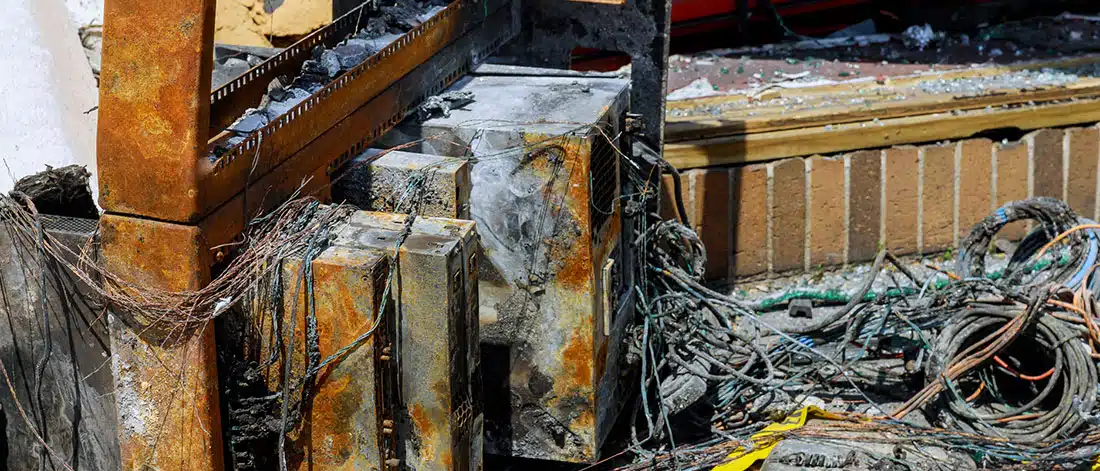

Document the Damage in Detail

After telling your insurance company about the damage, the next important thing to do is to record all the damage in detail. This helps show how much you’ve lost and helps with insurance claims.

- Take clear photos and videos of every damaged spot in the property. Get close-up pictures of specific damage and take wide shots to show the whole area that got damaged.

- Write down details about each broken item. Include what it is, the brand, when you bought it, and how much it’s worth. If you have receipts or proof that you own it, include those too.

- Keep notes on when the damage happened and what might have caused it, like bad weather or a machine breaking down.

This careful recording is important when you file claims and helps you get fair payment for your losses.

Track All Expenses Related to the Loss

Keep a clear list of all money spent after property damage. This is important to get money back from insurance and for taxes.

Business owners should write down repair costs, moving costs, new equipment, lost inventory, and how the damage affected the business.

Collect all bills, receipts, contracts, checks, and online payment records. Have a special system to organize these costs by type, date, and reason.

Other costs could be emergency help, cleaning up debris, professional repair services, and renting temporary equipment.

Take pictures or scan all money records and keep them safe both on paper and online. This helps you get the most from insurance, helps with any legal needs, and gives proof for tax reasons related to losses.